More than two-thirds of startups in India need to secure additional capital in the coming weeks to steer through the coronavirus pandemic, according to an industry report.

70% of startups in India, home to one of the world’s largest startup ecosystems, have less than three months of cash runway in the bank, and another 22% have enough to barely make it to the end of the year, according to a survey conducted by industry body Nasscom.

Only 8% of startups that participated in Nasscom’s survey said they had enough money to survive for more than nine months, the report published on Tuesday said.

As startups confront unprecedented times, many are thinking of taking dramatic steps to stay afloat. About 54% of some 250 respondents said they were looking to pivot to new business opportunities, and 40% said they wanted to diversify into growth verticals such as healthcare.

The cash crunch comes as investors become cautious about writing new checks to young firms in the country. In an open letter several prominent VC funds warned startups that they may find it especially challenging to raise new capital in the next few months.

For some startups, there are other factors at play, too. More than 69% of business-to-business startups, especially those operating in retail and fintech categories, say in the report that they are facing delays in payments from their clients.

This has left more than 50% of such startups to enforce pay cuts, reduction in marketing spends, and a quarter of them to switch to a lower-cost vendor to save money.

Startups operating in transport and travel sectors are also severely impacted, with 78% of respondents saying they were rethinking their business models and tweaking their products in accordance with the current scenario.

In a call with reporters on Tuesday, executives at Oyo unveiled new steps the budget lodging startup had taken at its hotels to ensure safety for operators and customers. They also said they were hoping that the government would allow more people to travel and stay at hotels again.

More than two-thirds of startups said they were looking for policies that eased regulations and spur government purchases. Many also requested relief in taxations for a few years.

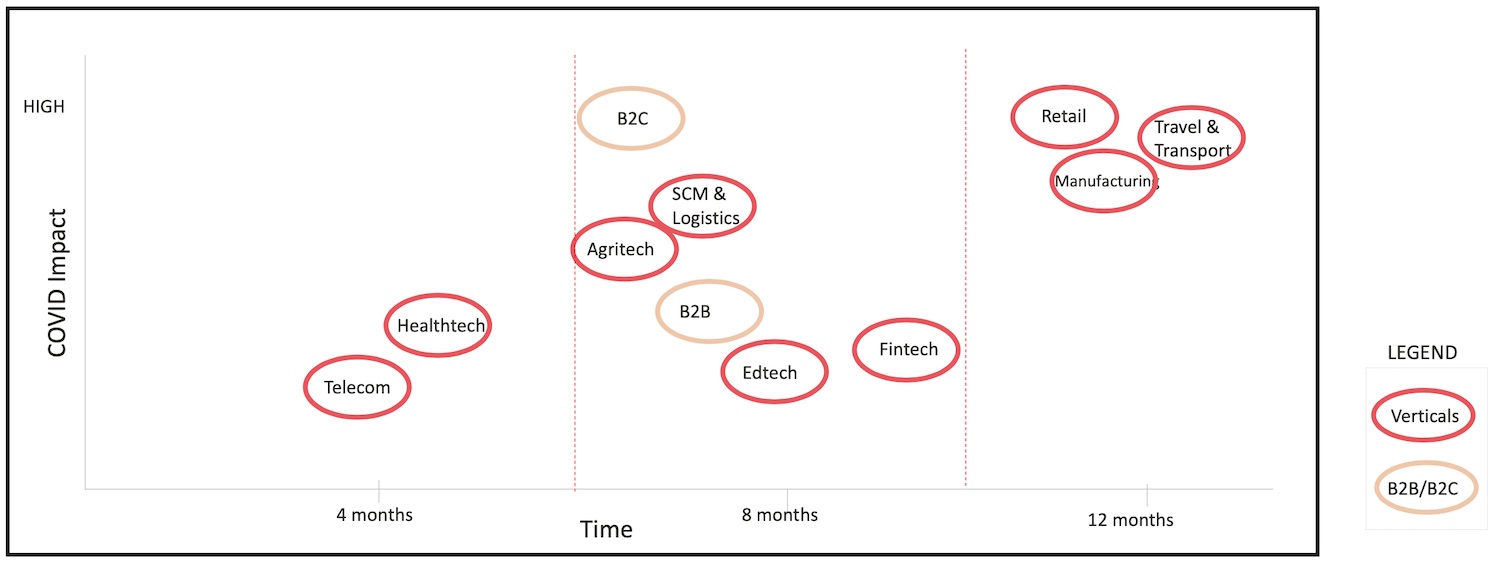

More than two-thirds of Indian startups believe the impact of coronavirus will linger for up to 12 months. (Nasscom)

Earlier this month, India announced a $266 billion stimulus package to help revive the stalled economy. On Saturday, Indian Finance Minister Nirmala Sitharaman said that startups too will be able to access some of this relief — though details remain sparse on how they should go about it.

Since 2017, India’s startup ecosystem has grown consistently. Last year, startups in the country raised a record $14.5 billion.

“Out of the blue, this flourishing growth saga has suddenly been hit by a roadblock… the COVID roadblock. There is no country, business or living being that has not been affected by the COVID pandemic. While governments have been working diligently to protect and save human lives, businesses have been hit and small businesses and start-ups have been the most affected,” said Debjani Ghosh, President of NASSCOM, in the report.

from TechCrunch https://ift.tt/2X8NFgB

No comments:

Post a Comment